Why You Should Care

Deep tech has quietly become the dominant force in venture capital. What was once a niche category for patient, specialized investors now commands 20% of all global VC funding - double its share from a decade ago.

The thesis is no longer controversial: the world's hardest problems - energy transition, computational limits, healthcare transformation, national security - will be solved not by software applications, but by companies built on fundamental scientific and engineering breakthroughs. Capital is flowing. Talent is migrating from big tech to hard tech. Governments are treating deep tech as strategic infrastructure.

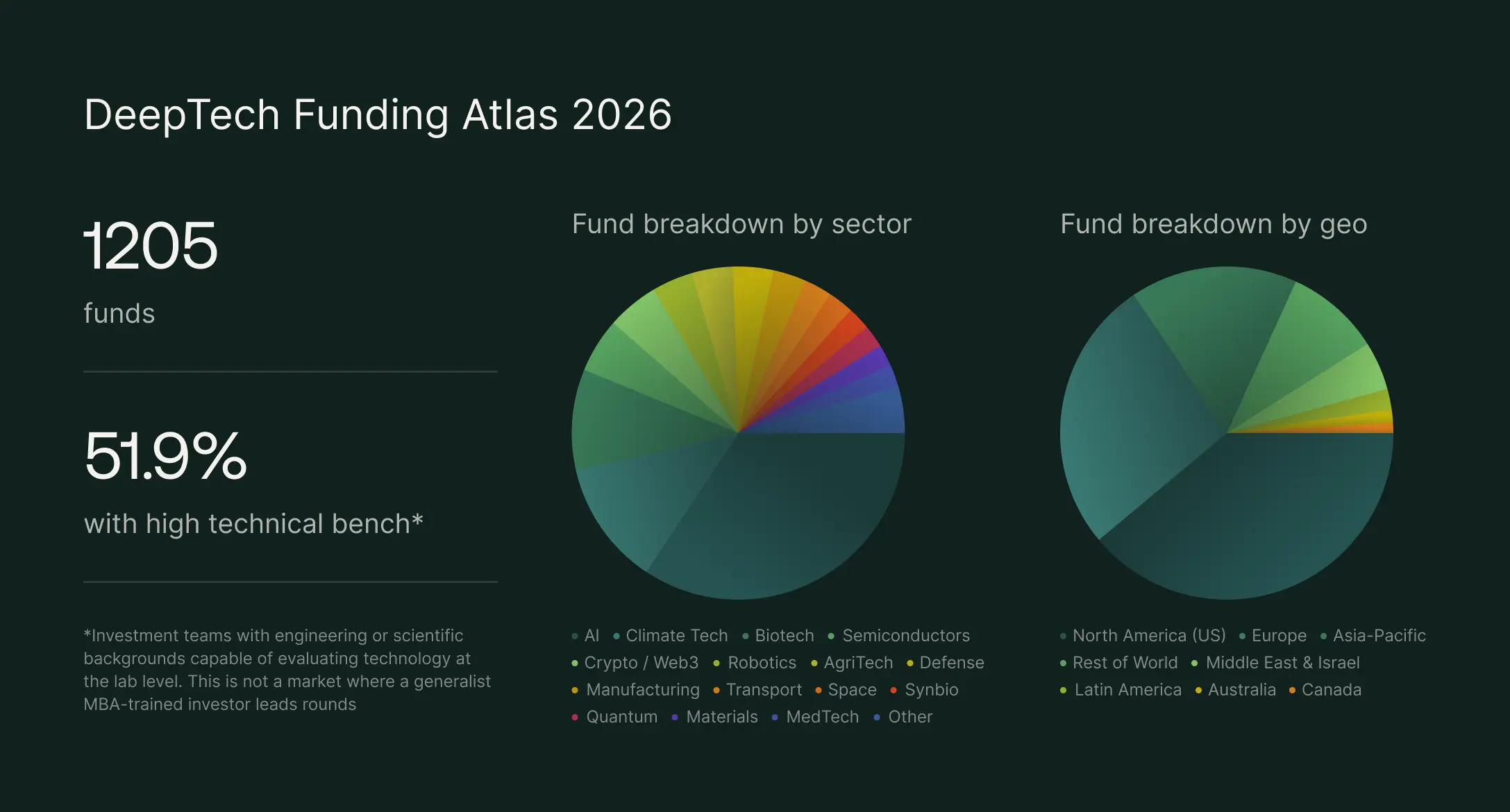

The complete investor database covering over 1,200 investors across all deeptech verticals, geos and funding stages.

Deep tech has arrived. But the playbook hasn't caught up.

The overwhelming majority of fundraising advice available to founders today was written for software companies - the metrics, the timelines, the pitch structures, the investor expectations. Yet deep tech operates under fundamentally different physics.

A software company reaches revenue in 12–18 months; a deep tech company may require five to seven years. A software company scales on $50–150 million; the top deep tech companies require $800+ million. And while thousands of generalist VCs fund software, only a small fraction of VCs globally have the genuine expertise and mandate to lead hardware-intensive rounds. In the recent years that pool has shrunk further as generalist crossover funds like Tiger Global and Coatue largely retreated from deep tech after 2021–2022 losses, making the market even more concentrated among specialists.

The consequences are severe: founders pitch investors who will never write the check, present metrics that don't resonate, model timelines that prove wildly optimistic, and dilute themselves unnecessarily before reaching value inflection. The founders who understand deep tech dynamics - the specialized investor base, the role of non-dilutive capital, the different milestones that matter - move faster, at better terms, with partners who can actually help. The difference isn't talent or technology - it's knowledge. This playbook exists to close that gap.

Deep Tech Funding in Numbers & Valuations

The Big Funding Picture

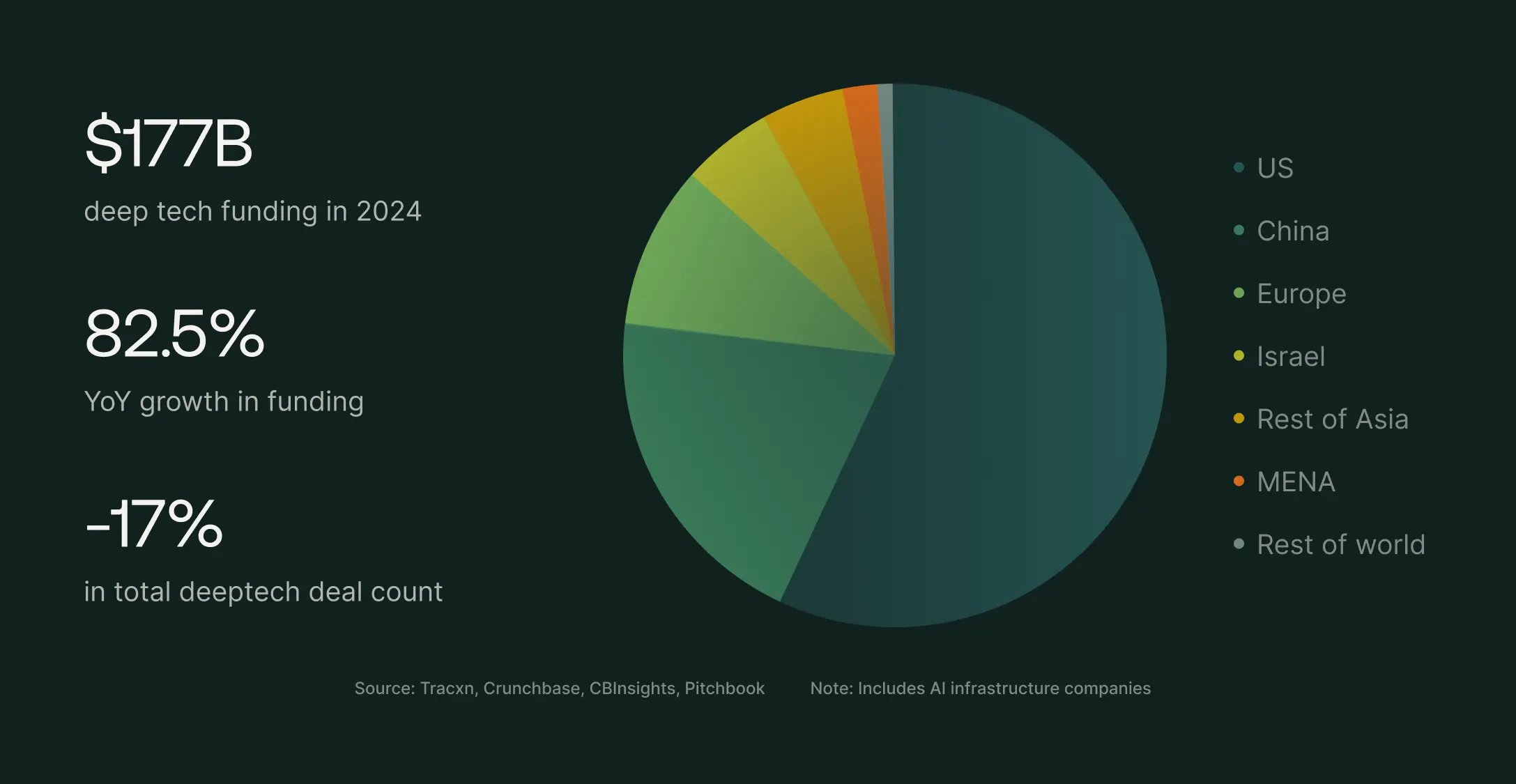

Deep tech is no longer a niche - it's one-fifth of all venture capital. The market has grown to $177 billion globally in 2025, an 82.5% year-over-year surge that outpaced the broader venture market growth (and that figure captures equity financing only, excluding corporate capital expenditure, government grants, or project finance - categories where deep tech commands multiples of its VC total).

The market is bifurcating: fewer deals, much larger rounds. Total deal count dropped 17% while funding rose 47%. Mega-rounds of $100M+ surged 77% and now capture 65% of all venture capital. The implication is clear: proven companies attract massive capital while unproven teams face an increasingly selective market.

Source: Tracxn, Crunchbase, CBInsights, Pitchbook. Note: Includes AI infrastructure companies

Sectors commanding most attention - and funding

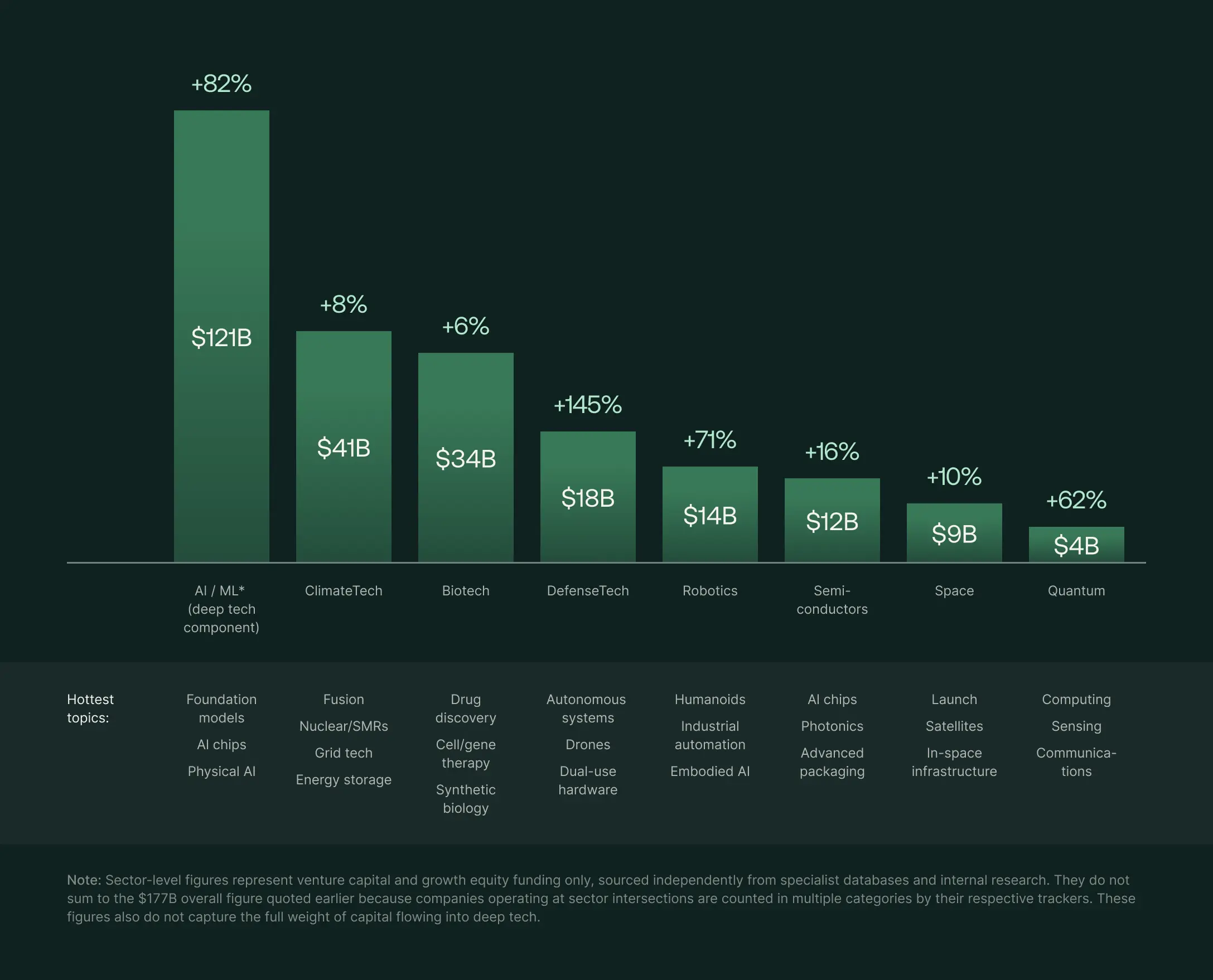

2025 was the year deeptech dominated venture capital. AI captured over a third of all global deeptech investment - an unprecedented concentration that reshaped capital allocation across every sector. Defense tech rode geopolitical tailwinds to its strongest year on record, posting 81% growth. Quantum computing more than doubled in Q1 alone, and robotics posted 70%+ growth YoY.

Not everything surged. Climate tech held its ground in aggregate, but the early-stage pipeline is thinning - a warning sign for the sector's next generation of companies. Biotech was volatile: down 20% in H1, then up 71% in Q3 as investors shifted toward companies with demonstrated clinical progress.

Source: Waveup DeepTech Survey 2026, Crunchbase, Carta, Pitchbook, Goldman Sachs, Bloomberg, Deloitte, McKinsey

Valuations & Round Sizes

Deep tech founders often assume they'll face punishing terms - technical risk and long timelines should mean investor-friendly deals, right? The data tells a different story. Series A valuations run 100%+ higher than software according to BDC - though this partly reflects that deep tech companies are typically 2–3 years older than software companies at the same stage. Rounds are often 50% larger.

The gap between different deeptech verticals at seed is relatively narrow - round size at seed averages $4–5M with average valuations sitting at $16–20M. At this stage, deep tech companies look broadly similar regardless of sector: small teams, early IP, and a thesis to prove.

The real divergence happens at Series A. Here, round sizes explode from $7M in climate tech to $30M+ in biotech and $50M+ in AI (with valuations ranging from $40M to $80M+). This is where sector economics start to dictate capital needs. AI companies raise large Series A rounds to secure compute infrastructure and hire expensive ML talent. Biotech needs to fund clinical trials and regulatory work. Climate tech, despite often higher valuations, raises the smallest Series A rounds (average at $7M) because capital deployment at this stage still revolves around pilot projects and site-level validation rather than full-scale buildout.

- AI commands the highest premiums, often reflecting the speed at which AI companies can demonstrate traction

- Defense and space benefit from dual-use pricing - investors pay up for government contract pipelines, treating them as de-risked revenue

- Biotech has the widest variance of any sector - valuations can jump 2–3x overnight when clinical milestones hit, but they can stall indefinitely when they don't

- AgriTech and climate are under pressure - both deal counts and valuations are declining, making this the toughest fundraising environment in deep tech. A significant share of climate tech and agritech rounds are closing at flat or down valuations - a dynamic largely absent from AI and defense

- MedTech is quietly posting record deal sizes - $7.7M average, the highest ever recorded. The sector is attracting serious capital with less fanfare than AI

Deep Tech Funding Trends & Key Lessons

Five structural shifts define the current environment. Founders who understand them will fundraise more effectively. Those who don't will wonder why the playbook isn't working.

- Capital is concentrating in proven winners. The era of funding promising ideas is fading. Investors want working prototypes, pilot customers, regulatory progress - tangible proof before they write checks. Founders without clear technical milestones face difficult fundraising conditions. The implication is straightforward: prove it early or struggle to raise.

- Specialist investors have displaced generalists. Relatively few firms have genuine deep tech expertise, and they drive most meaningful deals. Generalist VCs still take meetings, but they rarely lead rounds in sectors they don't understand. This concentration has deepened as generalist crossover funds (Tiger Global, Coatue) largely retreated from deep tech after 2021–2022 losses. Target the investors who actually fund deep tech - everyone else is a distraction.

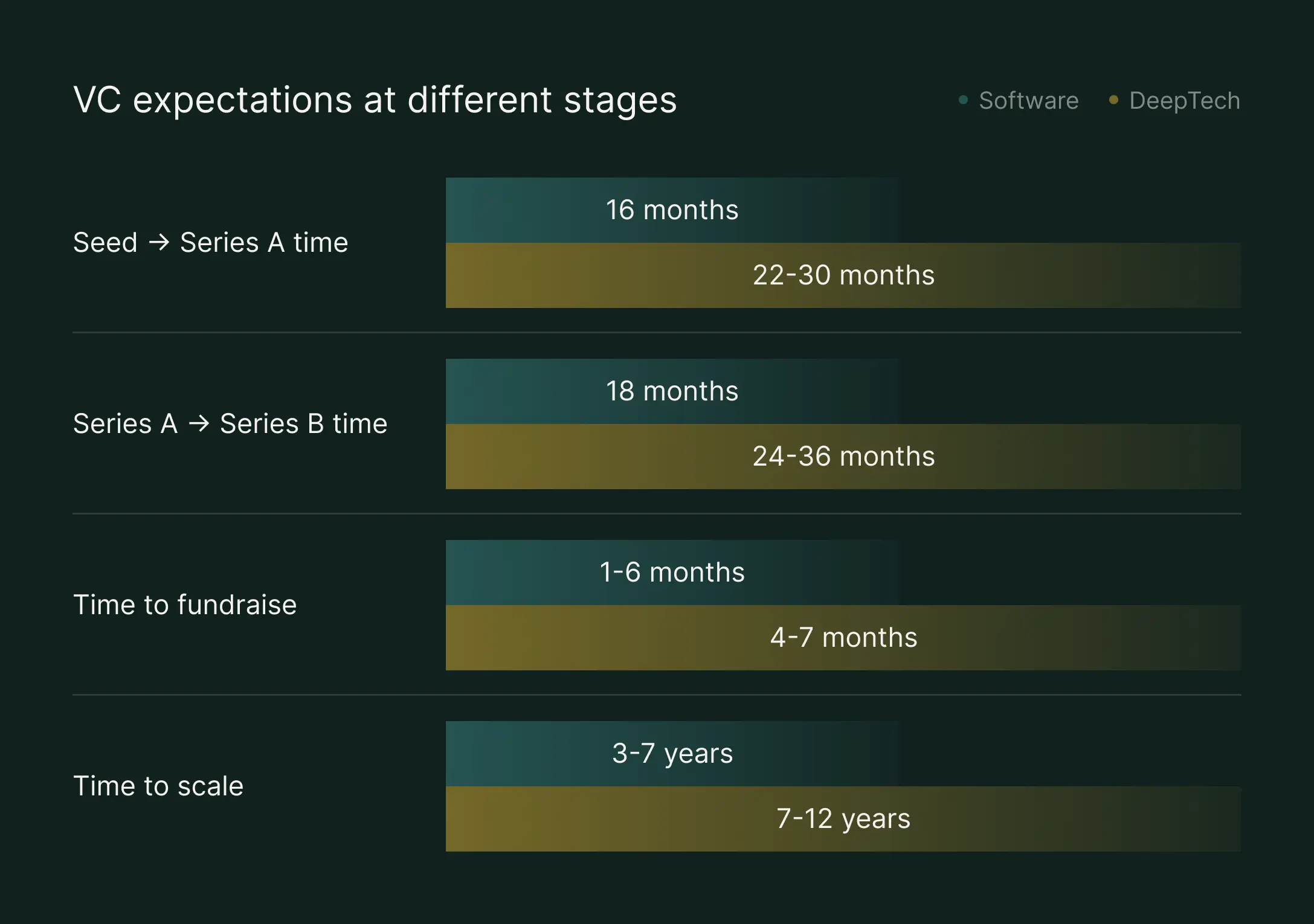

- Extended timelines are the norm, not the exception. Plan for 24–30 month fundraising cycles. Founders who budget for software-speed processes will run out of runway before they close.

- Exits are happening. M&A activity is accelerating, IPO windows exist for the right companies, and secondary markets are growing. The path to liquidity is real, even if it takes longer to reach - though exit multiples vary significantly by sector.

- The non-dilutive landscape is diverging. European grant programs are expanding and increasingly founder-friendly. SBIR/STTR was reauthorized in February 2026 through September 2031, with increased funding caps (Phase I up to $305K, Phase II up to $2.1M) and a planned set-aside expansion from 3.2% to 7% by FY2032. While the program's continuity is now secured, the future scope of broader government-backed non-dilutive funding remains uncertain.

Plan accordingly. Seed to Series A rounds stretch to 24–30 months versus 18 for software. The fundraising process itself usually runs at least 7–9 months. Among the top 100 deep tech companies (Bessemer's XB100), the average requires 9.2 years and $801 million to reach scale - though most deep tech startups will require significantly less capital and many will take longer. Founders who plan for software timelines will find themselves perpetually behind.

Source: Waveup DeepTech Survey 2026

The extended timeline isn't a bug - it's the nature of the asset class. Here's what's actually slowing things down:

- Technical risk demands more proof points. Investors won't underwrite science projects. They need working prototypes, pilot customers, regulatory milestones - tangible evidence that the technology works before they commit capital.

- Diligence runs deeper. VCs routinely bring in technical experts to evaluate claims most generalist investors can't assess. That adds weeks or months to every process.

- The investor pool is smaller. Fewer VCs genuinely understand deep tech, which means founders take more meetings to find the right partners. Expect a longer search.

- Hardware and regulatory timelines are fixed. You can't ship atoms as fast as code. Manufacturing has lead times. Approvals have their own calendar. No amount of hustle compresses these.

- Revenue takes longer to materialize. 35% more time and 48% more capital to generate meaningful revenue. Investors price this in - and so should founders.

Common Mistakes to Avoid

1. Applying SaaS Playbook to Hardware

For deep tech founders, it can be a company-killing move to just copy-paste advice for B2B SaaS. Understand from first principles what applies to you. You often can't "iterate fast" - hardware iterations cost money. Revenue timelines are longer, so avoid promising SaaS growth curves.

2. Underestimating Capital Requirements

Over half of startups often miscalculate first-year funding needs. In deep tech, this is fatal. Be realistic about prototyping and iteration costs, testing and certification, talent costs (PhDs aren't cheap) and time to revenue.

3. Targeting the Wrong Investors

Most VCs grew up in "software is eating the world" mindset. They're biased against capex-heavy models. Signs of a bad investor fit: no deep tech portfolio companies, no technical partners on staff, average hold period too short for your timeline.

Deep Tech Investor Expectations

Most fundraising advice is written for software. Deep tech operates on a fundamentally different logic - longer development cycles, heavier capital requirements, and a progression defined by technical de-risking rather than revenue growth. What follows is a stage-by-stage breakdown of what deep tech investors actually evaluate, from pre-seed through Series B. These are the benchmarks, team signals, and commercial milestones that matter in hardware, biotech, climate, defense, and frontier tech.

What Deep Tech Investors Actually Underwrite

Investors de-risk sequentially. Seed capital buys technical proof. Series A buys product-market signals. Series B buys the right to scale and commercial execution. Founders who understand what's being underwritten at each stage - and focus their narrative accordingly - close faster at better terms.

| Pre-seed | Seed | Series A | Series B+ | |

|---|---|---|---|---|

| Average round size | $0.5–4M | $3–8M | $8–20M | $20–100M+ |

| Team | 2–3 people (core technical co-founders). Deep technical expertise and ability to articulate the vision | 2–5 people (mostly technical). Strong first technical hires, demonstrated domain credibility and commercial awareness | 8–20 people (technical + first commercial hires). Proven ability to attract credible leaders across functions | 25–60+ people (full leadership team in place). First and second line of management hired |

| Product, Tech & IP | TRL 2–3. Concept to small-scale lab demo. Core invention identified, provisional IP filings | TRL 4–5. Lab demonstration in small-scale industrial setting. Provisional patents filed, clear claim to proprietary technology | TRL 5–6. Industrial pilot/PoC with path to full scale. Issued or pending patents, freedom-to-operate analysis complete | TRL 7+. Production-ready, focused on scale and efficiency. Patent portfolio with defensive depth |

| Commercial traction | None required. Problem validation interviews and proof the market exists | None required, but customer references preferred. The best companies show paid pilots or first LOIs signed | Revenue not required, but the best companies show $1M+ in early sales and/or strong pipeline. Validated hypothesis on revenue streams, pricing, LTV and margin profiles | Revenue expected ($1M+, though most demonstrate $10M+). Proven repeatable sales motion, clear playbook to scale GTM |

| Capital strategy | Grants, university partnerships, angels & select early-stage deeptech VCs | Grants, SBIR Phase I, university partnerships, angels & early-stage deep-tech VCs, corporate sponsors | SBIR Phase II, strategic partnerships, government contracts, deep tech VCs, generalist VCs, corporate sponsors | Government contracts, strategic debt, blended financing, generalist and deeptech VCs |

What Kills Deals at Each Stage

Each stage buys down a specific category of risk. Pre-seed validates the science. Seed proves it works beyond the lab. Series A demonstrates industrial viability and commercial interest. Series B proves you can scale manufacturing and sales profitably.

| Pre-Seed | Seed | Series A | Series B |

|---|---|---|---|

| Unclear technical / scientific differentiation | Results aren't repeatable outside lab | Tech doesn't work at an industrial scale | Manufacturing economics don't pencil |

| Founding team incomplete | No credible founder-market fit | Team can't hire beyond founders | Execution velocity slowing |

| No credible de-risking roadmap | IP position weak or contested | Unit economics unclear | Competition has closed the gap |

| Market too small / too crowded | Regulatory path not understood | No customer validation signals, no commercial traction despite time | Sales motion isn't repeatable |

Technology Readiness and the "Valley of Death"

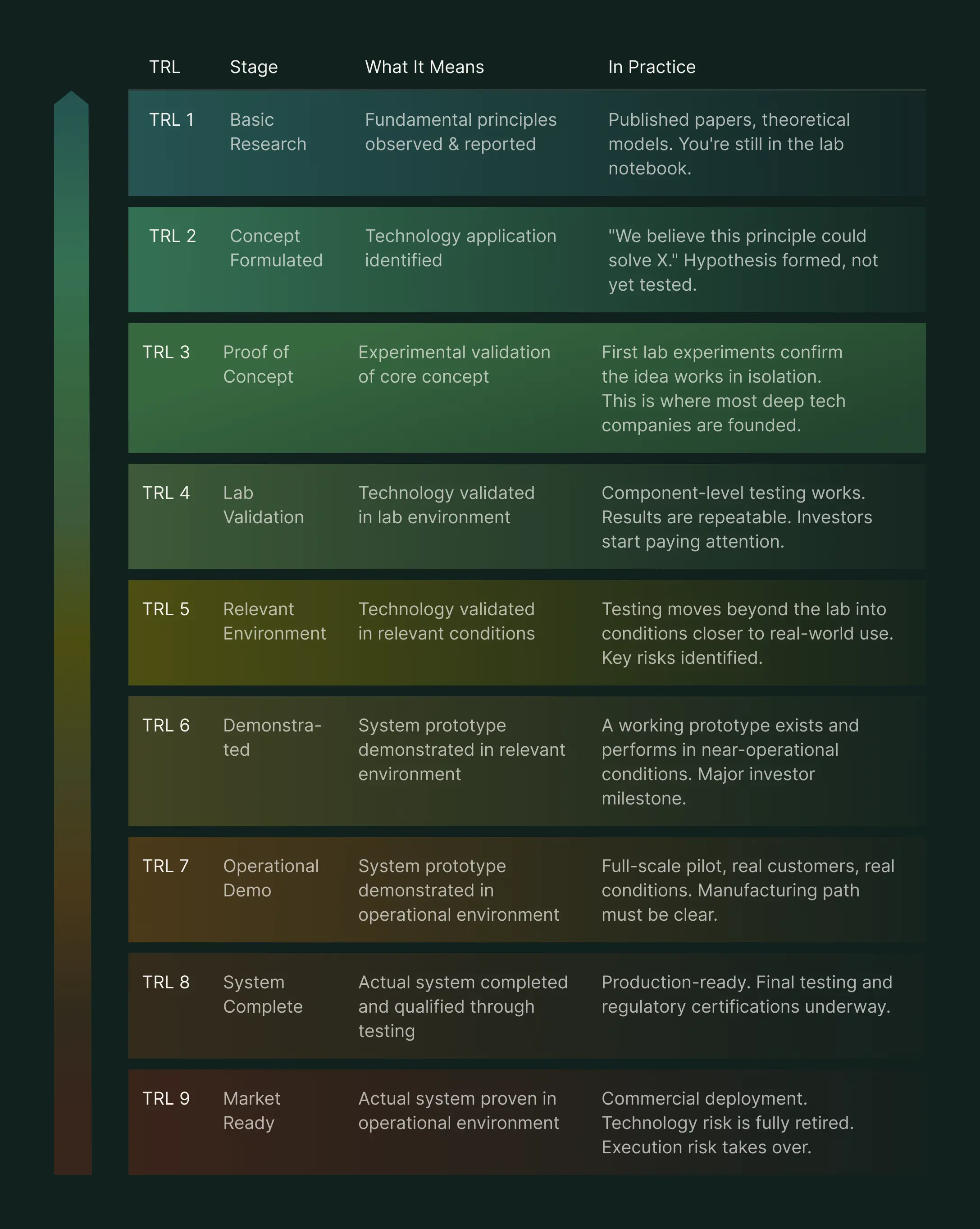

The path to commercialization in deep tech follows a rigorous sequence of Technology Readiness Levels (TRL). Technology Readiness Levels were developed by NASA in the 1970s to standardize how we measure a technology's maturity from initial concept to full commercial deployment. For deep tech founders, TRL is more than an academic framework - it's the language investors use to assess risk. Most deep tech VCs won't lead a round below TRL 3, and Series A typically requires TRL 5–6. By Series B, investors expect TRL 7+ with a clear path to production.

Most deep tech failures occur at the transition from TRL 4 (lab testing) to TRL 6 (field testing), often referred to as the technical "valley of death." This is where technology first encounters real-world operational conditions, and unforeseen integration complexities often arise. At this stage fundraising is often most challenging, precisely because the investor pool narrows: too mature for grant funding, too risky for growth-stage VCs.

It's worth noting that TRL measures technology maturity, not market readiness. That's where adjacent frameworks come in. Manufacturing Readiness Level (MRL) complements TRL by evaluating how close a technology is to being manufactured reliably and at scale - factoring in supply chain maturity, production processes, quality management, and cost control. A technology can sit at TRL 7 while its MRL remains low if the manufacturing process hasn't been figured out. This disconnect is where many deep tech companies stumble post-Series A: the technology works, but producing it affordably and repeatably is a different problem entirely. Smart investors evaluate both: TRL tells them whether it works, MRL tells them whether it can be built. Founders who can articulate progress on both axes present a more complete - and more fundable - picture.

How to Finance a Deep Tech Venture

Deep tech founders face a financing landscape that looks nothing like software. There is no single pitch deck that unlocks a seed round in six weeks. Instead, the path to capitalization runs through a layered ecosystem of non-dilutive grants, strategic corporate partners, family offices, and - eventually - venture capital firms with the technical conviction to lead hardware-intensive rounds. Understanding who funds what, when, and why is the difference between a company that survives the valley of death and one that dies waiting for the right check.

Where the Money Comes From at Each Stage

The funding mix evolves as companies mature. Early on, it's grants and angels. By Series B, it's institutional capital and government contracts. Knowing which sources to pursue - and when - keeps founders from wasting time on the wrong conversations.

| Pre-Seed | Seed | Series A | Series B | |

|---|---|---|---|---|

| Dilutive | Angels, university funds, pre-seed specialists | Deep tech seed VCs, syndicates | Specialist deep tech VCs, corporate venture | Growth-stage VCs, crossover funds, strategic investors |

| Non-Dilutive | University grants, SBIR Phase I, national innovation grants (BPI, EXIST, Innovate UK) | SBIR Phase II, Eurostars, early venture debt | DARPA, DIU, EIC Accelerator, Horizon Europe, venture debt | Government contracts, DOE loans, strategic partnerships, revenue-based financing |

| Who Leads | Angels or pre-seed funds | Specialist seed VCs | Deep tech VCs with domain expertise | Growth VCs with scale-up track record |

| Non-Dilutive as % of Total | Can be 50–70% | 30–50% | 20–40% | 10–20% |

Non-Dilutive Capital

The smartest deep tech founders delay dilution as long as possible. Before taking equity investment, they stack non-dilutive capital: government grants, university programs, competition prizes, and revenue-based financing. These instruments fund the earliest, riskiest work - lab validation, first prototypes, regulatory groundwork - without giving up ownership.

The options are substantial. In the US, the NSF's SBIR/STTR program alone distributes over $250 million annually to ~400 startups, with Phase I awards up to $305,000 and Phase II up to $1.25 million. The program was reauthorized through 2031 and now offers Strategic Breakthrough Awards of up to $30 million for post-Phase II companies ready to scale. In Europe, the EIC Accelerator offers up to €2.5 million in grants (with blended equity options on top), backed by a 2026 budget of €634 million. Germany's SPRIND - the country's federal agency for disruptive innovation - deployed €229 million in 2025 alone, using flexible instruments specifically designed to bridge the valley of death. In the UK, Innovate UK runs targeted programs with up to £38 million for robotics and autonomous systems and £18.5 million for semiconductors.

Defense-adjacent founders have access to DARPA, which funds through contracts, grants, and other transaction authorities with typical awards of $500,000 to $5 million. Climate tech founders can tap Breakthrough Energy's $3.5 billion portfolio, which provides philanthropic funding, catalytic capital, and connections for first-of-a-kind commercial demonstration projects.

University spin-out infrastructure is also stronger than most founders realize. Oxford Science Enterprises manages £1.1 billion dedicated to Oxford spin-outs. Cambridge Innovation Capital, ETH Zurich, and EPFL run comparable programs. Accelerators like IndieBio (SOSV) offer $525,000 in seed funding plus lab space for early-stage biotech - its 310 graduates have raised $3.6 billion in follow-on funding since 2015.

For companies with early revenue, non-dilutive debt instruments are an option. Companies like Lighter Capital offer $50,000 to $4 million in revenue-based financing with repayment tied to 2–8% of monthly revenue - no equity, no warrants, no board seats.

The principle is simple: use non-dilutive capital to de-risk the technology before negotiating equity terms.

Corporate Investors and First Customers

In the past year, over half of our deep tech clients received their first meaningful investment from a strategic corporate partner - often a future customer who sees direct commercial value in the technology.

Deep tech solves problems that corporations cannot solve internally: novel materials for automotive OEMs, AI inference chips for hyperscalers, synthetic biology for chemical giants, autonomous systems for defense primes. The corporation doesn't invest because they want a financial return. They invest because they need the technology to exist.

This makes corporate venture capital the second-largest source of early deep tech funding after traditional VC. The ecosystem is deep: Intel Capital has deployed over $20 billion across three decades. Samsung NEXT has backed 320 companies (including 18 unicorns). BASF Venture Capital has made 125 direct investments in chemical innovation, new materials, and clean tech since 2001. Lockheed Martin Ventures doubled its fund to back AI, robotics, quantum, and space systems. BMW i Ventures has produced 11 unicorns including Figure AI (humanoid robotics) and Boston Metals (green steel). Airbus Ventures, Shell Ventures, Bosch Ventures, and Merck's M Ventures each run focused programs aligned to their core industries.

For founders, the strategic investor dynamic cuts both ways. The upside: access to testing facilities, pilot programs, supply chains, and regulatory relationships that pure financial VCs cannot provide. The risk: exclusivity clauses, slow decision-making, and strategic misalignment if the corporate parent pivots. The best deep tech founders take corporate money with clean terms - no information rights that spook future investors, no exclusivity that locks out competitors, and clear IP boundaries.

Family Offices, Government Funds, and Long-Patience Capital

Deep tech's extended timelines - 5 to 10 years from lab to revenue - make it a natural fit for capital sources with longer time horizons than traditional VC funds. Family offices, sovereign wealth funds, and government-backed investment vehicles have increasingly moved into the space, often co-investing alongside VCs at Series A and beyond.

Government-backed funds have a median fund size of $483 million - larger than most specialist VCs. These investors bring patient capital and often serve as anchor LPs in deep tech fund vehicles.

Venture Capital Funds

Venture capital remains the primary engine of deep tech scale-up financing. But the VC landscape for deep tech is structurally different from software. The investor base is smaller, more specialized, and more technically demanding. Not every fund can underwrite a Series A for a quantum computing company or a fusion energy startup. The ones that can are concentrated, active, and increasingly well-capitalized.

The next section maps out the global deep tech VC landscape - 1,205 funds across 19 verticals - to understand who actually deploys capital in this space.

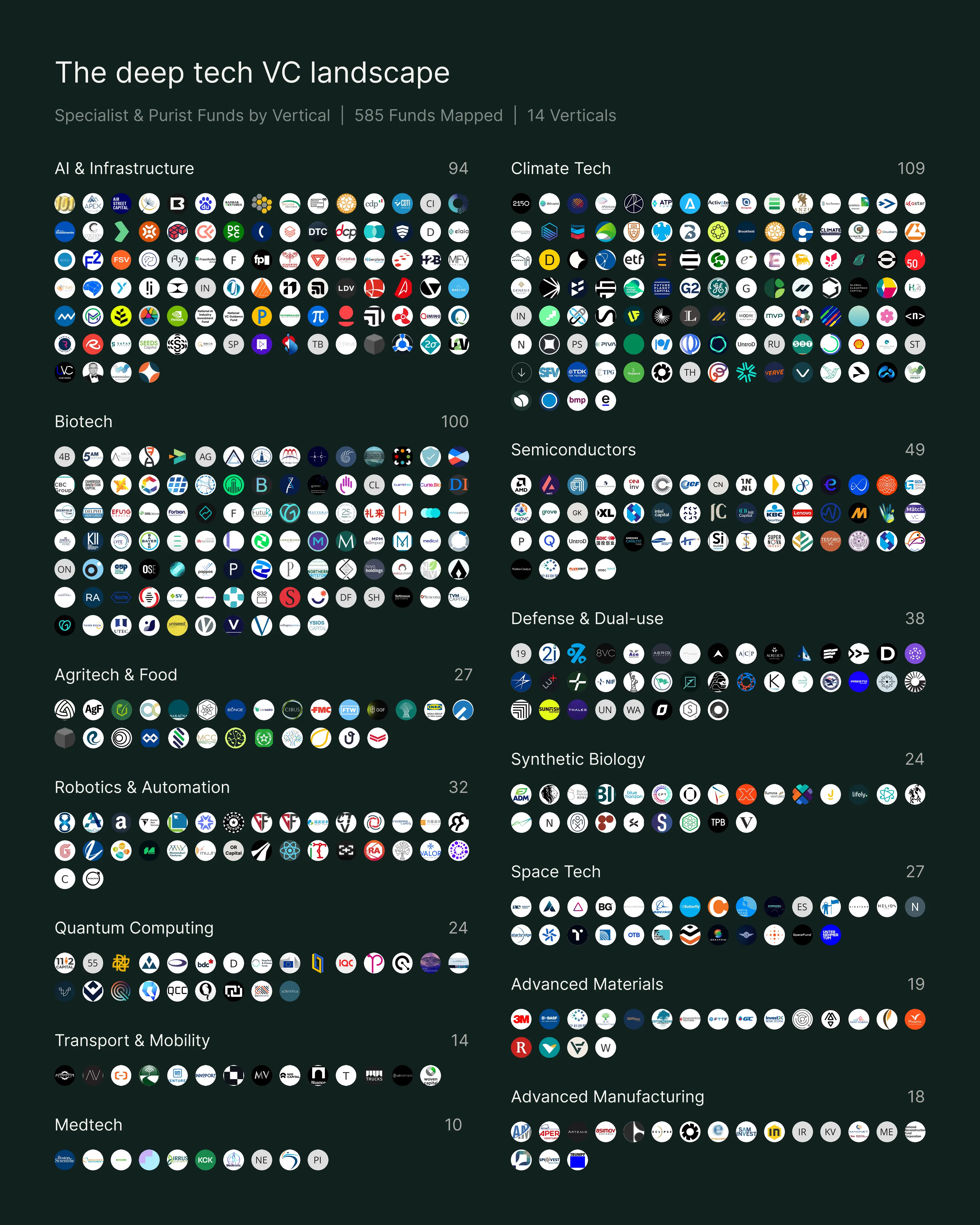

VC Investors Investing in Deep Tech in 2026

To support founders navigating deep tech funding landscape, we compiled and enriched a proprietary database of over 1,200 venture capital funds investing in deep tech - broken down by region, investment vertical, stage focus, fund size, and investor type. This is, to our knowledge, the most comprehensive open mapping of the deep tech investor ecosystem available today.

The database includes purist deep tech funds, specialist sector investors, generalist arms of major platforms, corporate venture capital, government-backed vehicles, university funds, and venture studios - across 19 verticals and 30+ countries.

| Type | Count | Meaning |

|---|---|---|

| Purist | 177 | Exclusively deep tech - won't invest outside hard science/engineering |

| Specialist | 481 | Focused on specific deep tech sectors (e.g., biotech-only, climate-only) but may have some non-deep tech deals |

| Generalist Arm | 247 | Deep tech arm of a larger generalist firm (e.g., a16z's bio fund) |

| CVC | 151 | Corporate venture capital (e.g., Shell Ventures, Salesforce Ventures) |

| Industrial | 45 | Industrial/manufacturing corporates investing in tech |

| Government | 57 | Government-backed funds (e.g., sovereign wealth, defense funds) |

| University | 28 | University-affiliated funds |

| Studio | 19 | Venture studios that build + invest |

The complete investor database covering over 1,200 investors across all deeptech verticals, geos and funding stages.

This investor database is just the starting point. In the past year alone, our team has been behind multiple fundraising rounds totaling over $200 million in deployed capital across hardware, biotech, defense, and climate ventures. We've guided companies from stealth to market, through first institutional rounds, through scale-up financing, and through exits.

We work hands-on with founders on fundraising strategy, deck and narrative development, financial modeling, go-to-market planning, and the full commercialization journey from lab to revenue. We've seen what works - and more importantly, what kills companies - across hundreds of deep tech firms.

If you're a deep tech founder preparing to raise, coming out of stealth, or navigating the path from prototype to product-market fit, get in touch. If you're an investor looking for deal flow in a specific vertical, stage, or geography - or want early access to companies before they hit the market - we can connect you to what's coming next.

Deep tech is not a category. It is a conviction - that the hardest problems are worth solving even when the path is longer, the capital requirements are heavier, and the uncertainty is real. The founders who build in this space don't get the luxury of moving fast and breaking things. They move deliberately and build things that last. The investors who back them aren't chasing momentum - they're underwriting the future before it's obvious. This report exists because we believe that future deserves better infrastructure: better data, better maps, better frameworks, and better access to the capital that makes it possible. If any part of this was useful to you, share it with someone who needs it. And get in touch if you would like to be included in the future reports - this ecosystem mapping will get more accurate with every participant who joins the conversation.